Flood Insurance Rate Maps & Flood Insurance

National Flood Insurance Program (NFIP) Information

In 1968, Congress created the National Flood Insurance Program (NFIP) in response to the rising cost of taxpayer-funded disaster relief for flood victims, and the increasing amount of damage caused by floods. The NFIP makes federally-backed flood insurance available in communities that agree to adopt and enforce floodplain management ordinances to reduce future flood damage. National Flood Insurance is available in more than 20,000 communities across the United States and its territories.

Management

The NFIP is managed by the Federal Emergency Management Agency (FEMA) and the Federal Insurance Mitigation and Administration (FIMA) Directorate. FIMA manages the insurance component of the NFIP and oversees the floodplain management aspect of the program.

Program Benefits

The NFIP, through partnerships with communities, the insurance industry, and the lending industry, helps reduce flood damage and helps to save the nation more than $1.1 billion a year in prevented flood damages. Further, homes constructed in compliance with NFIP building standards suffer less damage from floods than those not built in compliance. A study by the Multi-hazard Mitigation Council indicates that each dollar spent on mitigation saves society an average of $4.

Funding

The NFIP is self-supporting for the average historical loss year, which means that operating expenses and flood insurance claims are not paid for by the taxpayer, but through premiums collected as flood insurance policies. For more information on NFIP, visit the FEMA website.

Facts Everyone Should Know About the National Flood Insurance Program

Everyone lives in a flood zone.

- You don’t need to live near water to be flooded.

- Floods are caused by storms, melting snow, hurricanes, and water backup due to inadequate or overloaded drainage systems, dam or levee failure, etc.

Flood damage is not covered by homeowners’ policies.

- You can protect your home, business, and belongings with flood insurance from the National Flood Insurance Program.

- You can insure your home with flood insurance for up to $250,000 for the building and $100,000 for your contents.

You can buy flood insurance no matter what your flood risk.

- Whether your flood risk is high, medium, or low, you can buy flood insurance as long as your community participates in the National Flood Insurance Program (NFIP). Prince George’s County participates in the NFIP.

- It’s a good idea to buy, even in low or moderate risk areas: approximately 25% of all flood insurance claims come from low to moderate risk areas.

There is a low-cost policy for homes in low to moderate risk areas.

- For the Preferred Risk Policy, buildings and content coverage starts at $129 a year.

- You can buy up to $250,000 of coverage for your home and $100,000 of coverage for your contents.

Flood insurance is affordable.

- A $100,000 flood insurance premium would cost about $400 a year ($33 a month).

- In comparison, for a $50,000 loan at 4% interest, your monthly payment would be about $240 a month ($2880 a year) for 30 years.

Flood insurance is easy to get.

- You can get information about NFIP flood insurance online at floodsmart.gov. You can find flood insurance providers available for Maryland along with contact information.

- You may be able to purchase flood insurance with a credit card.

Contents coverage is separate, so renters can insure their belongings too.

- Up to $100,000 contents coverage is available for homeowners and renters.

- Whether you rent or own your home or business, make sure to ask your insurance agent about contents coverage. It is not automatically included with the building coverage.

Up to a total of $1 million of flood insurance coverage is available for non-residential buildings and contents.

- Up to $500,000 of coverage is available for non-residential buildings.

- Up to $500,000 of coverage is available for the contents of non-residential buildings.

There is usually a 30-day waiting period before the coverage goes into effect.

- Plan ahead. Don't be caught without flood insurance when a flood threatens your home or business.

Federal disaster assistance is not the answer.

- Federal disaster assistance is available only if the president declares a disaster.

- More than 90% of all disasters in the United States are not presidentially declared.

- Flood insurance pays even if a disaster is not declared.

Source: FEMA: NFIP

Note: Prince George's County residents receive a 25% reduction in flood insurance rates.

Community Rating System (CRS)

The Community Rating System (CRS) is a program started in 1990 under the NFIP. The program was designed to recognize and encourage community floodplain management activities that exceed the minimum NFIP standards. Under the CRS, flood insurance premium rates are adjusted to reflect the reduced flood risk resulting from community activities that meet the three goals of the CRS:

- Facilitate accurate insurance rating

- Promote awareness of flood insurance

- Reduce flood losses

There are 10 CRS classes: class 1 requires the most credit points and gives the largest premium reduction, while class 10 is the entry level into the CRS and carries no premium reduction. Prince George’s County is currently rated Class 5 under the CRS, which translates to a 25% reduction in flood insurance rates for local residents and businesses. The Class 5 rating places Prince George’s County in the top 3% of over 1,200 communities nationwide that participate in the CRS. For more information on the CRS, visit the FEMA website.

Cooperating Technical Partners (CTP) Program Activities

Under the CTP Program, the county has conducted and continues to conduct activities which utilize GIS-based tools. Such activities include:

- Completion of countywide GIS-based 2-foot topography using LIDAR technology. FEMA, the Maryland State Highway Administration, the Maryland-National Capital Park and Planning Commission and the County agreed on cost-sharing.

- Updating FEMA's Flood Insurance Study (FIS) and Flood Insurance Rate Map (FIRM). This endeavor will result in the production of the premier digital FIRM for the county. On September 30, 2010, FEMA released the preliminary FIS and DFIRM; FEMA proposed to issue a revised preliminary FIS and FIRM for the county in February 2013.On September16, 2016, this project came to fruition as the new FIRM's became effective.

- Conducting a technical review of FEMA map amendment (LOMA) and map revision (LOMR) requests.

- Conducting floodplain studies for developers using our GIS-based H&H models. Fees average approximately $2,500 for this service.

Is Your Property in a Flood Hazard Area?

Special Flood Hazard Areas are areas that will be inundated by the flood event having a 1% chance of being equaled or exceeded (100-year flood) in any given year. Smaller scale floods (50-year and 10-year) have a greater chance of occurring in any given year and can also pose a significant flood hazard to persons and property in close proximity to channels and streams. Additionally, floods larger than the mapped 100-year event can occur.

Flood Hazard Potential

First and foremost, you should become informed as to the flood hazard potential on your property. The Prince George’s County Department of Permitting, Inspections and Enforcement will review floodplain information and studies available in their files to determine the location of your property with respect to the floodplain as established in the Federal Emergency Management Agency (FEMA) Flood Insurance Rate Maps. You may contact the Prince George’s County Department of Permitting, Inspection and Enforcement at 301-636-2063 for assistance with this information.

Any information provided by the county does not constitute an assurance or representation that flooding may or may not occur on your property during any given event, but should assist you as a general matter in determining the need for flood insurance by assessing the extent of flooding potential on your property.

Flood Insurance Rate Maps (FIRMs)

The FEMA Flood Insurance Rate Map (FIRM) is the official map showing the community’s Special Flood Hazard Areas. This map is utilized as the basis to assess flood risk based on compliance with the minimum requirements for flood management under the NFIP and to determine if flood insurance is required for structure(s) on a property. Although the map is not property specific (e.g. no lot boundaries), by using the major roads and flooding sources for reference, users can get an idea of the flood risks in their area.

The map is available to view online at the FEMA Map Service Center or FEMA Floodplain Maps - Prince George's County. Additionally, the County site has an address search feature that allows a user to find the correct FIRM panel using their address in an online search tool (be sure pop-up blocker is turned off). After entering an address, a user may choose the interactive map options to see flood hazard data relative to the searched address.

Letters of Map Amendment & Revision (LOMA/LOMR)

In some cases, a lender determines that a property is in the Special Flood Hazard Area (SFHA), or 100-year floodplain, and requires the owner to purchase flood insurance. If the property owner wishes to dispute the fact that they are in the SFHA, they can apply for a Letter of Map Amendment (LOMA) or a Letter of Map Revision Based on Fill (LOMR-F), if fill placement is the basis of the request. Also, a Conditional Letter of Map Revision (CLOMR) or Letter of Map Revision (LOMR) may be required if a land development project would result in changes to the SFHA. Forms for this application process may be found on FEMA’s website.

You may also access tutorials designed to assist in the preparation of these forms at online-tutorials. This tutorial will guide you through the application and provide tips on filling out the forms.

Determination

Upon receiving a completed application, FEMA reviews property-specific information and makes a final flood zone determination for the property. Once an application is received with all the required supporting data, the LOMA or LOMR-F is normally issued within 60 days. If the LOMA or LOMR-F removes the SFHA designation from the property, it can then be presented to the lender as proof that there is no federal flood insurance requirement for the property. Bear in mind that even though a LOMA or LOMR-F may remove the federal requirement for flood insurance, a lender retains the prerogative to require flood insurance.

Elevation Certificates

Elevation certificates are prepared by surveyors and document the ground elevation, floor elevation, and general building characteristics for a structure in relationship to the Base Flood Elevation.

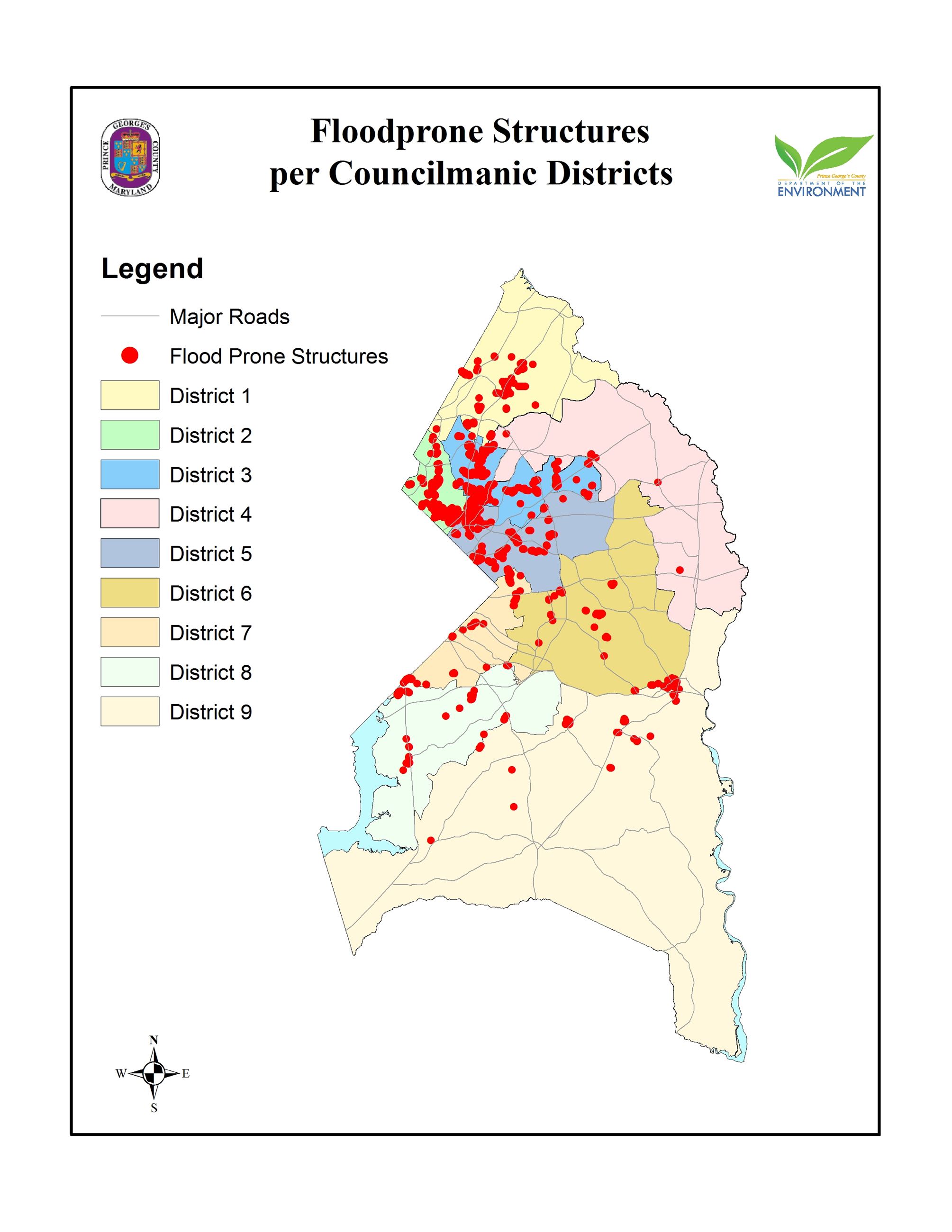

Known Floodprone Structures per Councilmanic District

Review a map depicting the known floodprone structures in the county.